Published on Australian Financial Review 18/03/2022 (Original Article Here, subscription required) – William McInnes

Investors looking to capitalise on the biggest surge in commodity prices in a generation will need to tread cautiously amid a volatile environment, as concerns over slowing growth play tug of war with supply shortfall fears.

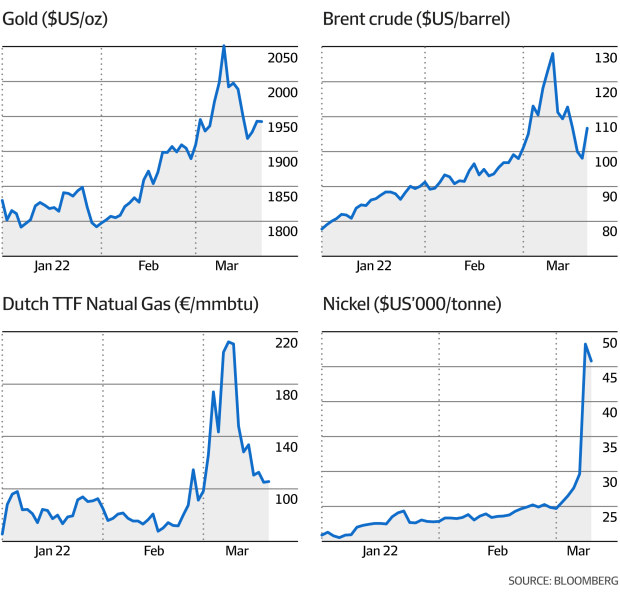

Energy, precious metals, base metals and bulk metals have all surged since the start of the year, with many commodities hitting record or multi-year highs, amid fears of inflation and the supply fallout caused by the conflict in Ukraine.

Since the start of the year, the MSCI World Index has fallen more than 11 per cent, while the MSCI World Metals and Mining Index has risen close to 10 per cent.

While there’s no doubt the short-term spike in commodities in the past few weeks has been driven by fears of a supply shortfall from Russia – one of the biggest metals and energy producers in the world – prices were rising before that.

Mining and energy stocks have been rallying since November, with the world emerging from its COVID-19 coma, driving demand for metals, oil, gas and coal.

BHP Group and Rio Tinto have risen more than 6 per cent since the start of the year, amid strong iron ore and copper prices, with investors hopeful they’ll back up their dividend windfall from the last six months of 2021.

In February, Santos reported record free cash flow for 2021, while Woodside Petroleum more than tripled its underlying profit when Brent Crude prices averaged just over $US70 a barrel. In 2022, the price has averaged $US92 a barrel.

While the surge in raw commodity prices and resource equities has created some short-term volatility, investors still believe there are opportunities to ride the potential start of a decade-long boom.

Equity prices lag

Broadly speaking, the rally in raw commodity prices hasn’t been matched by share price rallies in most producers, leaving room for share prices to rally as earnings forecasts get upgraded.

“Commodity producers haven’t done nearly as much as commodities have year-to-date, and they’ve actually lagged significantly,” says Ben Cleary, portfolio manager of the Tribeca Natural Resources Fund.

“If you look at oil producers, Santos and Woodside are only pricing in about $US65 a barrel crude at their current share prices, which is way below spot price.

“There’s a pretty good valuation margin for error in equities still because they just haven’t moved as much and that could lead to material earnings upgrades in the sector.”

While the price of Brent Crude has rallied close to 30 per cent since the start of the year, even after its significant fall in the past week, Santos is up less than 10 per cent.

Cleary says this makes the local energy sector one of the most attractive propositions in the middle of the commodity price surge.

“We like energy because it is very undervalued, particularly in Australia,” he says.

“Santos is an absolute standout given they’re also decarbonising at a rate of knots and most of the uranium stocks screen very cheap versus their global peers too.”

Katana Asset Management portfolio manager Romano Sala Tenna says his firm has rotated into energy and commodity stocks, benefiting from the rally in price.

“If you picked out one in particular, it would be coal because met coal prices are over $US600 a tonne, which is off the scales,” he says. “Even with some of those other prices pulling back, coal just hasn’t.”

Mineral Resources, OZ Minerals, Woodside Petroleum and Coronado Global Resources are all inside Katana’s top 10 holdings.

“Across the board, oil prices have pulled back, but in the scheme of things, it’s still at an extraordinary price,” he says.

“You’ve seen a bit come out of oil and gas, but the outlook for these stocks is very robust, even if you don’t get back to where we were.”

The underpricing of equities hasn’t just been in energy stocks.

The nickel price soared to a record high of $US100,000 a tonne last week, but the share prices of major nickel miners such as Nickel Mines, IGO and Western Areas have barely responded.

“It’s been pretty frustrating,” Cleary says. “Nickel Mines, Mincor and IGO are pricing about $US15,000 a tonne nickel at current valuations.”

Cleary says he expects share prices will begin to reflect the price of the underlying commodities more accurately in the months to come.

“There has definitely been a bit of selling of winners in global markets to fund margin calls for other sectors, and that’s something you tend to see early doors,” he says.

“Sometimes it can just take a little while for it to play out, and I’d expect those earnings to start to come through, and then you’ll see genuine decoupling and outperformance.”

Near-term caution

Not every investor is convinced that now is the time to reload on equities, however, with some warning demand destruction will begin to eat away at prices.

“I think there’s clearly a lot of parts to grapple with because even before what happened in Russia, we were grappling with risks of slowing growth,” says Tom Shelmerdine, metals and mining analyst at T. Rowe Price.

“What we tend to see in these scenarios is the higher commodity prices go, the risk of demand destruction becomes more prominent.”

Shelmerdine says energy prices are sitting at their highest levels since 2008 and 2011, which both preceded a period of economic slowdown.

“We’re getting a bit more cautious around where we’re investing,” he says.

“Where we’re more comfortable is through the China-centric commodities like iron ore. China runs a different race, and it will quickly react to a slowing domestic economy.”

Volatile

While many investors think there’s more to come from most commodity stocks, they’ve been quick to show a level of caution too, saying volatility in the sector is the highest it’s been in a long time.

“Resource markets are volatile at the moment as investors digest the implications of the Ukraine conflict, commodity supply risk, surging inflation, rising interest rates and the risk of slowing global growth,” says David Franklyn, chief investment officer at Argonaut Funds Management.

“From a tactical perspective over recent months we have skewed our portfolio to the larger, more liquid resource stocks, pushed our cash weighting up and lifted our exposure to the oil and gas sector as prices rallied.”

Katana Asset Management has also been nimble in its portfolio management through the volatility of the past few weeks.

“We’ve seen some pretty crazy things happening in commodities, so we’ve taken some profits in the last week because it’s very dynamic and much more volatile than we’re used to,” Sala Tenna says.

“We’re having to be very nimble because we’re seeing very large price movements on a weekly basis.

“We think we’ve probably just gone through the retracement period, so now we’re starting to rebuild some of these positions again.”

Some investors are positioning their portfolios towards gold, betting the geopolitical tensions that have driven commodity prices to near-record levels are unlikely to abate in the near-term.

“We believe that geopolitical risks will continue to grow into the future, and as such we maintain an exposure to quality gold companies as a hedge against this uncertainty,” Franklyn says.

“We currently have a weighting to gold of just under 20 per cent.”

Long-term thinking

Even with prices sitting at their highest levels in years, investors still appear confident the long-term structural trends around electrification will mean base metals and other “transition” commodity stocks remain good investments.

“Strategically, we continue to see the ‘energy transition’ thematic as the key resource sector driver over the next decade and have positioned our portfolio accordingly,” Franklyn says.

“Over 50 per cent of the portfolio is invested in companies exposed to copper, nickel, lithium and uranium.”

Regal Investment Management chief investment officer Phil King has suggested resource stocks are at the beginning of a decade-long boom, with neglected avenues of new supply and increasing demand for commodities set to drive gains well into the 2030s.

“These commodity themes are multi-year and investors have been saying it could be a decade-long boom for resources,” Cleary says.

“The next few years should be very strong as we see deficits across most commodities. The resource nationalisation on the back of Russia will only add to those deficits, and it might go on for a long time.”

While some commodity prices have soared to unsustainably high levels in the short-term, investors still believe prices can remain strong for the next few years, even if they retreat slightly.

“Nickel is having a moment, as is copper and the other base metals,” Sala Tenna says.

“And yes, the war has created some [metals] euphoria short-term, but outside that you still see very tight markets. You’ve had underinvestment in the sector and demand is now recovering.”

But T. Rowe Price’s Shelmerdine warns investors need to be cautious. “We still think in the longer term there’s structural demand around some of these commodities,” he says.

“But I think you just have to watch for the risks of demand destruction before we look at longer-term issues.”